Match Group & The App Store Battles

Match Group & The App Store Battles

Analyzing Regulatory Attacks on the App Stores and the Consequential Impacts on Match Group's Finances

Abstract

App Stores, in particular Apple’s App Store and Google Play, are coming under increased fire for extracting what’s deemed “supra competitive margins” from in-app purchases (IAPs). The stores intermediate between app users and app developers, providing systems of distribution and security while charging commissions on IAPs (historically at 30%).

App developers have long claimed App Stores have extracted these profits through anticompetitive means, e.g. by implementing anti-steering provisions or prohibiting alternative app stores from operating on particular mobile operating systems.

Regulators have recently increased efforts to limit App Store power, e.g. by proposing legislation requiring mobile operating systems to permit multiple app stores or by prohibiting anti-steering provisions.

Match Group, in particular, pays between 17 and 19% of its revenue to App Stores (with roughly 80% going to Apple). The company recently announced that (1) it expected an increase in the proportion of its revenue going to App Stores and (2) withheld profit guidance pending more clarity on future App Store charges. Yet as App Stores come under increasing fire, Match Group’s long-term prospects are looking brighter.

This post examines those prospects and finds, among other things, that Match Group’s gross and operating margins may increase by 11 percentage points with increased regulation governing App Store practices (or likewise decrease by roughly comparable percentages if Google Play were to implement its anti-steering provisions as Apple does).

I. Introduction

It would be hard to devise a better business than Apple’s App Store. In the Epic v. Apple matter, Epic’s expert calculated the App Store’s operating margin to be over 75%. Apple disputed the expert’s calculations, primarily on the grounds that it doesn’t allocate operating expenses to internal divisions (e.g. the App Store). But the judge found that Apple’s internal reporting (which is not publicly disclosed) was consistent with the 75% estimations.

Apple thus extracts an incredible amount of value by mediating between apps and users. Ordinarily, competition might be expected to erode these margins. Yet Apple effectively prevents such competition, per the judge’s decision. Through the anti-steering provisions in its Developer Program License Agreement (“DPLA”), Apple forces users to pay through the app store even though cheaper alternatives might have otherwise been made available. And by providing only one distribution mechanism—i.e. its App Store, and not alternative stores like Google Play—apps have no choice but to comply with the DPLA in order to reach Apple’s userbase.

Granted, it’s somewhat disingenuous to view the App Store as a standalone business. It’s incredible margins are only made possible by virtue of its hardware products which deliver a gross margin of just over 30%. And even Apple’s total services segment operates at a gross margin of less than the App Store’s estimated margin. (See the Apple breakdown in the chart below.)

But the point remains: Apple can take a cut from all in-app purchases (“IAPs”) from apps distributed on its devices in exchange for nominal operating expenses, thereby earning phenomenal margins.

As a consequence of Apple’s “supracompetitive margins”, as the Epic v. Apple decision characterized, Apple’s App Store and Alphabet’s Google Play are coming under increasing public criticism and regulatory attacks.

Match Group is one of the biggest critics, particularly since it currently pays roughly 19% of its revenue to app stores, 80% of which goes to Apple. Barry Diller, IAC chairman, said companies like Match Group are “overcharged in a disgusting manner.”

The article below focuses first on regulatory attacks on IAPs and then considers the impact on Match Group and its financial results.

II. Regulatory Attacks on App Store Commissions

Apple’s App Store and Google Play are being attacked from various jurisdictions across the world.

In the United States Senate, Sens. Blumenthal, Blackburn, and Klobuchar introduced the “Open App Markets Act” which would require Apple and Google to allow third-party apps and app stores.

South Korea’s parliament recently enacted legislation banning app stores from forcing developers to use their payment systems.

In Utah v. Google LLC & affiliates, 37 states that Google Play extracts a 30% commission on in-app purchases through “anticompetitive tactics to diminish and disincentivize competition in Android app distribution. Google has not only targeted potentially competing app stores, but also has ensured that app developers themselves have no reasonable choice but to distribute their apps through the Google Play Store.”

A federal judge sitting in the Northern District of California found that Apple’s anti-steering provisions violated California’s Unfair Competition Law (as explained in Part III infra).

Apple and Alphabet have both offered nominal concessions, e.g. dropping commission rates to 15% for developers earning less than $1M. Alphabet has repeatedly postponed enforcement of its anti-steering provisions, most recently to early 2022, and will reduce subscription revenue charges from 30% to 15% in early 2022.

III. Epic v. Apple

The headlines covering the Epic v. Apple decision centered around the opinion’s catchiest line, i.e. that “Apple is [not] an illegal monopolist.” The “illegal monopolist” language was perceived as a litmus test on Apple’s market power.

In fact, the decision was much more nuanced. The judge issued a mix-ruling.

In Apple’s favor, the judge dismissed Epic’s claims under federal and state anti-trust law and found in favor of Apple’s claims for breach of contract.

Epic’s claims under federal and state antitrust law failed as “[g]iven the trial record, the Court cannot ultimately conclude that Apple is a monopolist under either federal or state antitrust laws.”

Epic’s hotfixes enabling alternative payment mechanisms breached various provisions of the Developer Licensing Agreement (“DPLA”), including those prohibiting developers from embedding links within their applications to external sites which would enable customers to use “purchasing mechanisms other than in-app purchase” and those agreeing not to “provide, unlock or enable additional features or functionality through distribution mechanisms other than the App Store.” As a remedy for the breach, Epic was required to pay Apple commissions due under the DPLA, i.e. 30% of revenue derived from its subvert payment mechanisms.

In Epic’s favor, the judge held that:

Apple’s anti-steering provisions violate California’s Unfair Competition Law as they deprive consumers of information concerning pricing and prevent substitution among platforms.

The Court wrote, “Apple contractually enforces silence, in the form of anti-steering provisions, and gains a competitive advantage,” and elaborated:

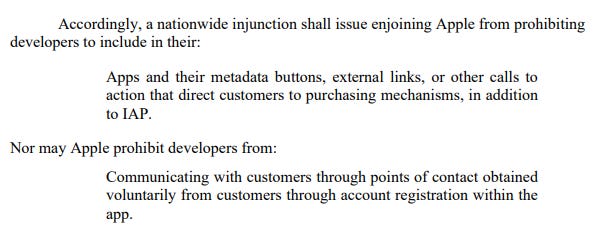

To remedy the violation, Apple as ordered Apple was required to permit alternative payment mechanisms in iOS.

The court ruled that the injunction applies nationwide as conduct occurring outside California nonetheless harms California residents. That is, to provide California residents with full information on pricing and with true opportunities to switch between platforms, Apple must eliminate anti-steering provisions nationwide. Whether California has the authority to apply its law nationwide will likely be litigated on appeal, but the rationale (although not fully fleshed out in the decision) does make sense. Developers operating outside California may not have incentive to link alternative payment mechanisms if Apple implements the change only to users residing in California.

The injunction is set to apply as of December 9, 2021 although Apple will certainly move to stay pending appeal.

IV. App Store Changes & Impact on Match Group’s Financial Results

Match Group’s Current IAP Payments

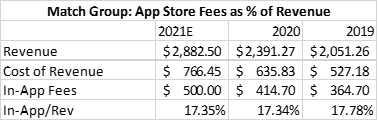

Match currently pays between 17% and 18% of its revenue to the App Store and Google Play.

(The 2021 revenue estimate is the guidance’s mid-point and the in-app fees are CFO Gary Swidler’s estimates (per a WSJ article.)

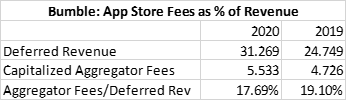

These figures are roughly in line with Bumble’s.

(Both firms defer subscription revenue and amortize on a straight-line basis over the duration of the subscription. Likewise, both firms capitalize and amortize IAP fees associated with particular contracts on the same duration.)

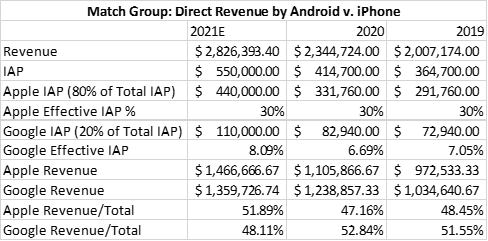

Match recently disclosed that roughly 80% of its IAP fees go to the App Store and only 20% go to Google Play. Assuming all sales through iPhones are charged with the App Store’s 30% rate, we derive the total sales from iPhones versus Android.

Match Group: Apple v. Android Users

Google Play, which has continued to allow firms to embed alternative payment mechanisms in their apps (despite repeated threats to end the workaround), effectively takes only 6.5% of sales through Android.

Android subscribers are thus far more valuable to Match Group than iPhone users. We can break subscribers into Apple v. Android buckets assuming 72% of all international subscribers are Android users.

Using these subscriber allocations, we see that Android subscribers’ net revenue rates (i.e. revenue minus IAP fees) are 25% higher than Apple subscribers’ (and the conclusion would hold even if you assumed, fairly, that Apple subscribers’ ARPU materially exceeded Android subscribers’).

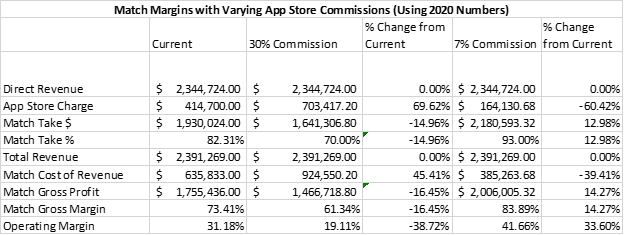

Margin Sensitivity to IAP Rates

You can also see the difference in values between Android v. iPhone users by comparing Match’s gross margins as would exist if all revenue were taxed at Apple’s rate (30%) or Google Play’s rate (7%).

A 30% charge on all revenues would result in a 61% gross margin and 19% operating margin, whereas a 7% charge would result in an 84% gross margin and 42% operating margin.

There’s little surprise, then, that Match is one of the loudest voices against app store commission rates.

V. Outlook

Match Group’s Outlook

In its Q3 2021 call, Match said it expects IAP fees to take 19% of its 2021 revenue, up from 17% in 2020. There are a few possible dynamics here.

Apple users comprise an increasing proportion of its subscriber base.

A la carte features (as opposed to subscriptions) comprise an increasingly large proportion of its direct revenue compared to subscription revenue.

Direct revenue will comprise an increasing proportion of its total revenue.

Match withheld EBITDA guidance for 2022, citing uncertainties in how future IAP fees will be charged.

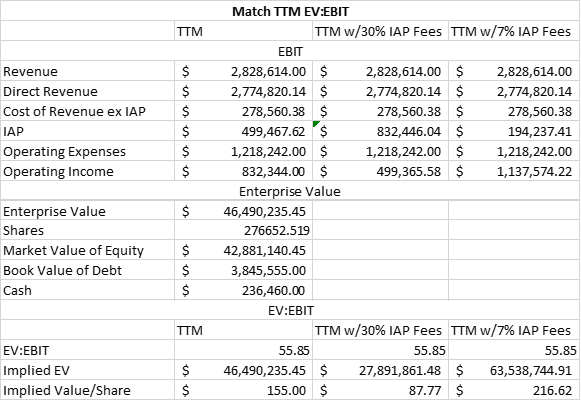

Valuations

As a shorthand for valuation impacts, let’s assume that Match’s current EV:EBIT ratio applies in either of the two extreme scenarios (all direct revenue being taxed at 30% or 7%).

There’s a 38% upside if effective IAP fees are reduced to 7% of revenue, and likewise a 42% downside if all revenue were taxed at 30%. These figures aren’t entirely predictive and you should form your own valuation, but the point is Match is highly exposed to effective IAP fees. If you see these fees decreasing over time, Match’s margin will likely increase as might its enterprise value.

Concluding Thoughts

Given all the pressure (including regulatory heat) directed at app stores, I don’t see how the App Store and Google Play can maintain the status quo. In the most likely scenario, I see the app stores maintaining 30% commissions on all IAPs while allowing links to alternative payment processing systems.

The effective IAP rate will drop. By my calculation, less than 25% of Android users pay through Google Play. The remaining users take advantage of Match Group discounts offered through alternative payment mechanisms. Apple users might have different price sensitivities, but the risk to the App Store and the reward to Match Group remain.